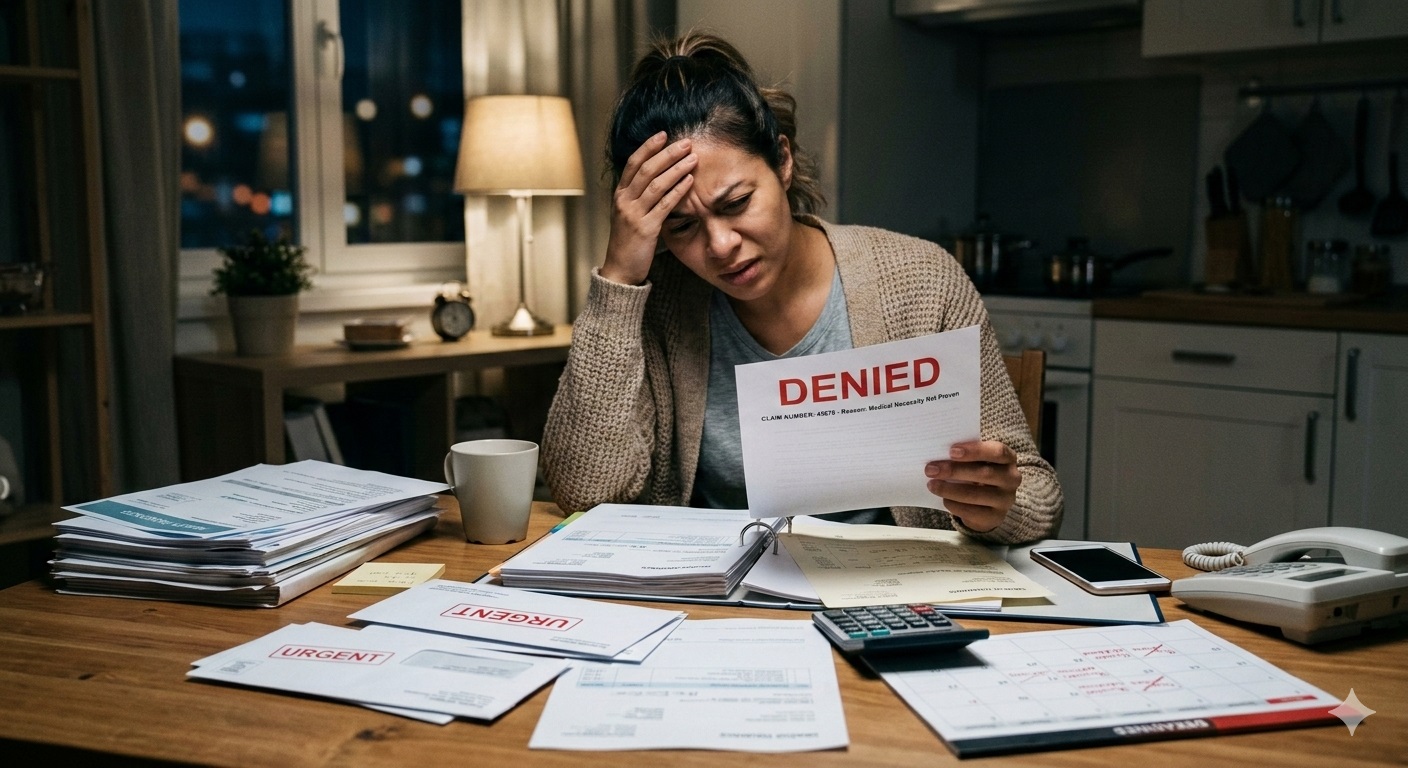

What Every Policyholder Must Know

Millions of Indians pay health insurance premiums every year believing that when

illness strikes, their insurer will stand by them. Yet a growing number of policyholders,

especially senior citizens, find themselves in a bewildering and exhausting battle for

rightful reimbursement. This article examines a real-world pattern of claim disputes,

explains the rights available to policyholders under Indian law, and outlines a step-bystep

path to resolution.

The Pattern: How Legitimate Claims Get Stuck

Claim disputes in health insurance typically arise from one or more of the following

situations:

- A clerical or typographical error in medical documentation (such as duration

of symptoms) that the insurer treats as grounds for rejection. - Requests by the insurer for ‘prior treatment records’ for a condition that was

acute and newly diagnosed. - Repeated, circular demands for the same documents without a clear final

decision on the claim. - Unreasonable classification of an acute illness as a ‘pre-existing disease’ based

on vague references to general age-related discomfort. - Absence of any proactive engagement by the insurer — no callbacks, no direct

resolution, only generic auto-responses.

These patterns are not random failures. They represent a systemic problem in how

some insurers manage reimbursement claims, particularly for elderly policyholders

who are less likely to escalate. Understanding these patterns is the first step to

protecting yourself.

Your Rights as a Policyholder

1. The Right to Timely Settlement

Under the IRDAI (Protection of Policyholders’ Interests) Regulations, 2017, an

insurance company is required to settle or reject a claim within 30 days of receiving

the last relevant document. If additional investigation is required, the claim must be

resolved within 45 days. Any delay beyond this entitles the policyholder to interest on

the outstanding amount.

2. The Right to a Reasoned Decision

An insurer cannot simply ‘keep asking for documents’ indefinitely. Every decision —

whether partial, complete, or a rejection — must be communicated to the policyholder

in writing with clear reasons. Demanding documents that do not exist (e.g., prior

consultation records for a newly diagnosed condition) without providing a final

decision is not compliant with regulation.

3. The Right to Have Errors Corrected

If a claim was initially declined due to a clerical error in a hospital document — such

as a wrong date, incorrect duration of symptoms, or a typographical mistake — and the

treating doctor issues an official correction letter, the insurer is obligated to reconsider

the claim on that corrected basis. The original rejection does not stand once the error

has been formally rectified by the issuing authority.

4. Protection Against Pre-Existing Disease Misclassification

Indian courts and IRDAI have consistently held that a condition must be properly

diagnosed and documented to be classified as a pre-existing disease. Vague references

in a patient’s history — such as ‘general back pain for two years’ noted by a general

physician — cannot automatically make a distinct and serious surgical condition (like

spinal canal stenosis requiring decompression surgery) a pre-existing disease. The

insurer must prove, with medical evidence, that the condition existed prior to policy

inception.

5. Portability Protections

Policyholders who have maintained continuous health insurance coverage — including

across different insurers — are entitled to portability benefits. This means that waiting

periods and certain exclusions for pre-existing conditions may be waived or reduced

based on prior coverage history. Continuity of coverage is a right, not a privilege.

When Things Go Wrong: The Escalation Path

Step 1 – Internal Grievance with the Insurer

The first step is to raise a formal written grievance with the insurer’s Grievance Redressal

Officer (GRO). By regulation, the insurer must acknowledge within 3 working days and

resolve within 15 days (extendable to 30 days with justification). Keep all your grievance

reference numbers. If the insurer provides only generic auto-responses and fails to

resolve the matter, move to the next step.

Step 2 – IRDAI’s Bima Bharosa / Integrated Grievance Management System (IGMS)

If the insurer fails to resolve within 30 days, or you are unsatisfied with the resolution, you

may register a complaint with the Insurance Regulatory and Development Authority of India

(IRDAI)

IRDAI’s Policyholder Protection Department will direct the insurer to respond within a

prescribed timeframe. Retain IRDAI’s case reference number for subsequent use.

Step 3 – Insurance Ombudsman

The Insurance Ombudsman is the most powerful and cost-free redressal mechanism available to individual

policyholders for disputes involving amounts up to Rs. 50 lakh. There are 17 Ombudsman offices across India.

A complaint can be filed if:

- The insurer has rejected the complaint or not resolved it within 30 days of receiving the complaint, OR

- The policyholder is not satisfied with the resolution offered.

The Ombudsman’s award is binding on the insurer (though the complainant may choose to reject it and seek

other remedies). The process is free, relatively fast (30-90 days), and does not require legal representation

Step 4 – Consumer Forum

Policyholders may also approach the District Consumer Disputes Redressal

Commission (for claims up to Rs. 50 lakh), State Commission (up to Rs. 2 crore), or

National Commission (above Rs. 2 crore) under the Consumer Protection Act, 2019.

In insurance disputes, courts routinely award not only the claim amount but also

compensation for mental agony and costs.

What Documents You Should Keep

Whether or not you are currently facing a dispute, every health insurance policyholder

should maintain:

- All original policy documents, premium receipts, and policy certificates.

- Every OPD slip, prescription, and consultation paper — from the very first

doctor visit for any condition. - All laboratory, imaging, and diagnostic reports.

- The complete hospital admission file: case papers, consent forms, discharge

summary, final itemized bill. - Every written communication with the insurer — emails, letters, WhatsApp

messages (where applicable) — with timestamps. - Grievance reference numbers and insurer responses.

A Special Note for Senior Citizen Policyholders

Elderly policyholders are disproportionately affected by claim disputes. They may have

limited familiarity with digital grievance systems, face difficulty travelling to insurer

offices, and may lack the stamina to sustain prolonged correspondence battles. If you

are a senior citizen or have an elderly family member with a health insurance policy,

consider:

- Designating a trusted family member or friend as the person managing all

insurance correspondence. - Ensuring all communications are in writing (email or registered post) so there

is a documented trail. - Requesting the insurer’s senior citizen helpline or dedicated support channel

in writing. - Not accepting verbal assurances — any commitment by the insurer must be in

writing. - Being aware that the Ombudsman can also award compensation specifically for

harassment caused to a senior citizen.

Key Principles to Remember

To summarize, if your health insurance claim has been delayed or denied:

- You are legally entitled to a decision within 30 days of submitting the last

relevant document. - A clerical error in a hospital document, once corrected by the treating doctor,

cannot continue to be the basis for rejection. - Vague references to general discomfort in a patient history do not automatically

make a surgically treated condition a ‘pre-existing disease.’ - There is no obligation to provide documents that do not exist. If there are no

prior treatment records, a declaration and a certificate from the treating doctor

is sufficient. - The Insurance Ombudsman is a free, effective, and legally backed mechanism.

Do not hesitate to use it. - Your silence and patience will not resolve a bad-faith claim. Escalation through

proper channels is your right.

Share

Post a comment Cancel reply

Related Posts

February 24, 2026

Money Recovery Under Indian Law

Who This Article Is For : Maybe you lent a friend money and they stopped…